If smart money doesn't do film, someone forgot to tell BlackRock

Wall Street started treating film like an asset class. And why family offices are treating film the same way they used to treat contemporary art

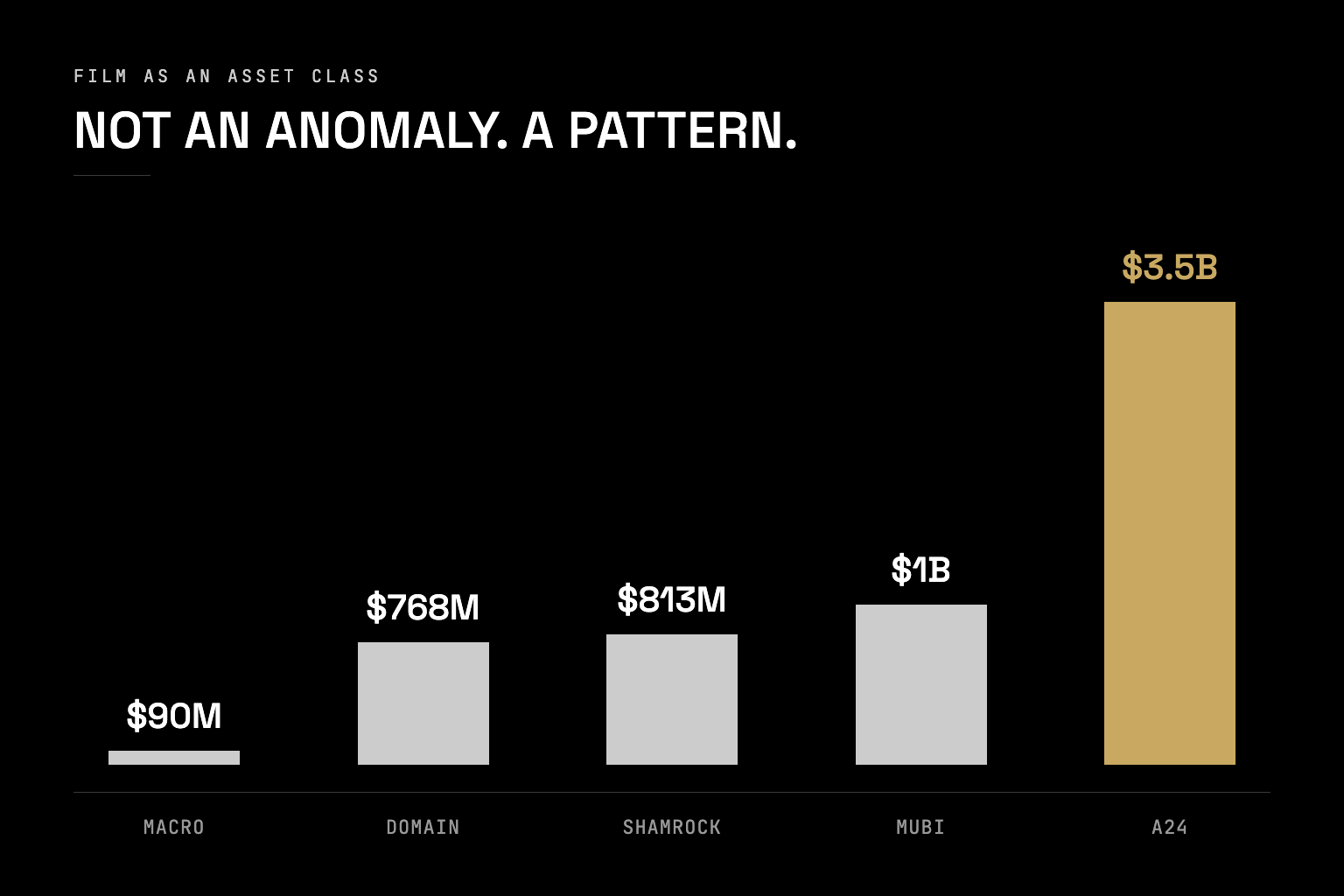

In 2023, BlackRock Alternatives put $90M into MACRO, a film company founded with the explicit thesis that Black-centered storytelling is a massively underserved market. The round was led by BlackRock, with Goldman Sachs Asset Management and HarbourView Equity Partners alongside.

Not a philanthropic arm. BlackRock Alternatives. The same division that manages institutional capital for pension funds and sovereign wealth vehicles.

If smart money doesn’t do film, someone forgot to tell BlackRock.

The more honest framing is this: sophisticated capital has always followed genuine market gaps. What’s changed is the visibility. MACRO’s raise wasn’t an anomaly - it was the most legible data point in a pattern that’s been building for years.

And it kept happening. In June 2024, Josh Kushner’s Thrive Capital led a round that valued A24 at $3.5B, up 40% in two years. A year later, Sequoia put $100M into Mubi at a $1B valuation.

Then there are the funds built for exactly this. Shamrock Capital, which started as the investment office for Roy E. Disney’s family, closed an $813M content fund in 2026, backed by pension funds and endowments, structured to buy film cash flows the way other funds buy real estate. Domain Capital closed $768M for the same purpose the same year. None of this is charity. It’s asset allocation.

Plan B Entertainment built its track record on films that other companies passed on. “12 Years a Slave.” “Moonlight.” “The Big Short.” Not a diversity mandate. A selection thesis: find the stories audiences are hungry for before the market knows it. Plan B sold a majority stake to European conglomerate Mediawan in 2022. Mediawan didn’t buy that company for its B-movie output. Mediawan is backed by KKR. Since buying Plan B it has rolled up a run of quality producers across Europe, including the team behind “Slow Horses” and “The Power of the Dog”, and paid roughly $900 million for Peter Chernin’s company in early 2026. Private equity running a deliberate play on prestige production, not a one-off.

Element Pictures in Ireland operates on a similar logic. Ed Guiney and Andrew Lowe describe themselves as not driven primarily by commercial success, then produce “Room,” “The Favourite,” “Poor Things” - which grossed $117.6M globally. Killer Films has been running the same play for thirty years: Christine Vachon identified early that underserved audiences are underserved because no one served them, not because they don’t exist. That’s a business model, not idealism.

HarbourView Equity Partners, one of MACRO’s co-investors, has since done it twice more: Mucho Mas Media in 2024 and the Oscar-winning animation studio Lion Forge in 2025. The same investor doing it three times is a thesis.

The institutional interest has a second driver that’s less discussed. ESG - the environmental-social-governance investing category - is collapsing under its own weight.

BlackRock supported 47% of environmental and social shareholder proposals in 2021. By 2024, that number had dropped to 4%. By 2025, under 2%. US sustainable funds have now seen net outflows for fourteen consecutive quarters. In 2024, seventy-one ESG funds merged or liquidated in the same year only ten new ones launched. In January 2025, BlackRock walked out of the Net Zero Asset Managers Initiative entirely, and JPMorgan and Franklin Templeton followed within weeks.

ESG failed because it was built wrong. Negative screening - filtering out the worst actors in existing public companies - was never a mechanism for creating anything. It was a marketing mechanism that collapsed when political pressure arrived and greenwashing got called out.

The investors who went through that cycle and came out the other side are asking a different question now. Not “how do we filter what we own.” But “how do we fund what gets built.”

Film is one of the clearest answers available. When a film about climate resilience reaches thirty million people across theatrical, streaming, and educational distribution, it created something. An ESG-screened portfolio didn’t create anything. It just didn’t hold shares in the wrong companies.

Family office capital is moving toward what Goldman Sachs’ 2025 Family Office Investment Insights Report calls the “passion plus return” bucket. In one survey of ultra-wealthy investors, nearly 40% planned to increase their passion-asset allocation over the next five years, more than the share planning to increase traditional investments. Sports ownership already draws 25% of family offices. At the ultra-high-net-worth level, collectors now put 28% of their wealth into art, up from 15% a year earlier.

Film belongs in that bucket, and the distinction from sports team ownership is meaningful. Sports teams carry operational costs, municipal politics, labor negotiations, and stadium debt. A film investment is cleaner: the asset is the IP, the revenue windows are contractual, and the cultural product has global distribution potential from day one. It also has something a stadium doesn’t - it can still be watched in forty years.

The “stewardship not extraction” framing is what lands with the third generation of family office capital. Their grandparents funded concert halls and university buildings. Perspective-expanding cinema is the contemporary equivalent: accessible globally, permanent in cultural memory, and structured as an equity investment rather than a donation.

I’ve watched investors come to film after ESG cycles, after crypto cycles, after realizing that negative screens and speculative tokens are two different ways to feel like you’re doing something without actually building anything. The ones who stay are the ones who understand that cultural infrastructure compounds differently than other assets.

A film doesn’t depreciate the way a stadium does. It doesn’t dilute the way a token does. And unlike an ESG fund, it actually produces something.

The institutional validation is the least interesting part. The more interesting part is the question it leaves open: if BlackRock and Mediawan are at the table, what’s the right structure for the next layer of capital to enter alongside them?

That’s where the independent producer conversation starts getting interesting. And the window for that conversation is wider right now than most investors have priced in.