The $3M film that only needs $1.1M from you

When investors see a $3M film budget, most of them are looking at the wrong number.

The number that matters is equity-at-risk: the slice of the budget that’s actually exposed if the film fails. On a well-structured $3M indie, that figure lands somewhere between $750K and $1.5M. The rest of the budget comes from a stack that most pitch decks explain badly.

Here is how that stack actually works.

Layer 1 - Tax credits.

Tax credits are the boring layer. Boring is the point: this is the only money in film that arrives whether or not anyone buys a ticket.

British Columbia refunds part of every dollar spent on BC labour, and it stacks higher than most investors think.

Start with the floor. The Production Services Tax Credit pays 36% of eligible BC labour, and the federal services credit adds 16% on top. The two don’t reduce each other. That’s 52% of qualifying BC wages back as a refundable government check - refundable meaning the government pays it out in cash even if you owe no tax.

Then it stacks. Shoot outside metro Vancouver and a regional credit adds 6%. A distant location adds another 6%. Visual effects and post-production qualify for the DAVE bonus at 16%. A distant-location, effects-heavy production pushes the combined credit up to 80% of eligible BC labour.

What that means for an investor: labour runs roughly 50-60% of a budget, so the credit comes back as something like 35-45% of the total budget.

On a $3M genre thriller, shot at a distant BC location with VFX work and the bonuses carry the cashback is roughly $1.2M. Independent of box office, independent of whether the film ever reaches a festival. More about Tax Credit and how to maximize it here.

Layer 2 - Pre-sales and minimum guarantees.

A minimum guarantee is exactly what it sounds like: a territorial distributor commits to pay a fixed amount - say $500,000 for US rights, $100,000 for UK - against delivery of a finished film. That commitment is made before production starts. The MG is a real cash advance, often borrowed against by a bank once the contract is signed.

When investors see the budget line for “pre-sale,” they sometimes read it as projected revenue. It isn’t. It’s a contracted advance from a buyer who has already evaluated the package - script, cast, producer track record - and committed in writing.

Layer 3 - Sales agent advance.

A reputable sales agent occasionally provides an advance against their commission. Smaller than the pre-sales but real: another $100,000-$200,000 in the stack without additional equity dilution.

MGs and sales advances are great additions to your package and pitch, it’s proof that it isn’t just you thinking the film is good. Someone with real money on the line already believes it’s marketable.

Put the layers together.

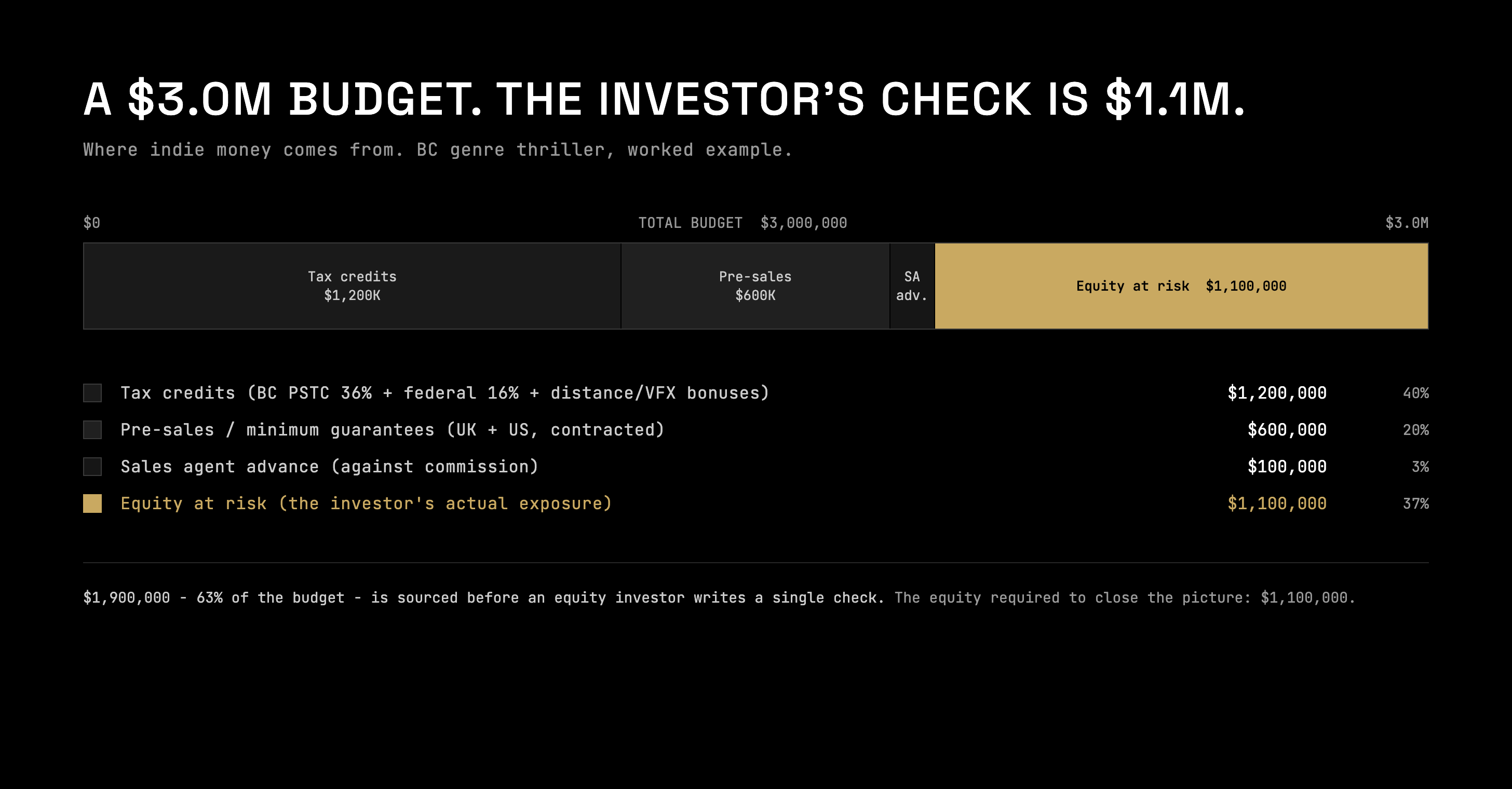

Take the $3M BC thriller worked example I use when structuring deals. Tax credits bring in roughly $1,200,000. UK and US pre-sales total $600,000. Sales agent advance adds $100,000.

That’s $1,900,000 - 63% of the budget - sourced before an equity investor writes a single check. The equity required to close the picture: $1,100,000.

When investors see $3M and walk away from the table, they are often walking away from a deal where their actual exposure was $1M to $1.5M - against a project that already had a collection account CAMA (a neutral account where every dollar of revenue lands, more on that in part 3), a completion bond (insurance that the film actually gets finished), and signed distribution commitments from territorial buyers who evaluated the same materials the investor was shown.

That’s the gap between perception and structure.

The perception is that the film is a $3M binary bet on whether audiences show up opening weekend.

The structure is that a well-packaged indie is a $1M-$1.5M position with a tax credit floor, contracted pre-sale commitments, and a recoupment waterfall - the contractual order money comes back in - that puts the equity investor’s principal ahead of the producers.

Not every film is structured this way. A lot of them aren’t. But when the stack is assembled correctly, equity-at-risk is a materially different number than the budget. The investor who knows to ask for it is operating with a different frame than the one who looked at the cover page and stopped there.

Knowing the size of your check is one half of the math. The order that check comes back in is the other.