Film as an Alternative Asset

How cinema compares to the alternatives you already own

Educational, not financial advice. Numbers are sourced and dated. Talk to your own advisor and an entertainment lawyer before you invest in anything, mine included.

Most investors file film in the wrong drawer

Ask someone where film sits as an investment and you get one of two answers. Either it’s a gamble for rich people who want to walk a red carpet. Or it’s a blank stare, because they never knew you could invest in a film at all.

Both are wrong.

I produce independent films. That puts me on the other side of the table from the investor, building the thing your capital would back. So I wrote the comparison I’d want a sharp investor to run on me. Not a pitch. A map. Where does film actually sit next to venture capital, crypto, real estate, and angel deals?

The five questions every alternative asset has to answer

Strip away the story and every alternative asset answers the same five questions:

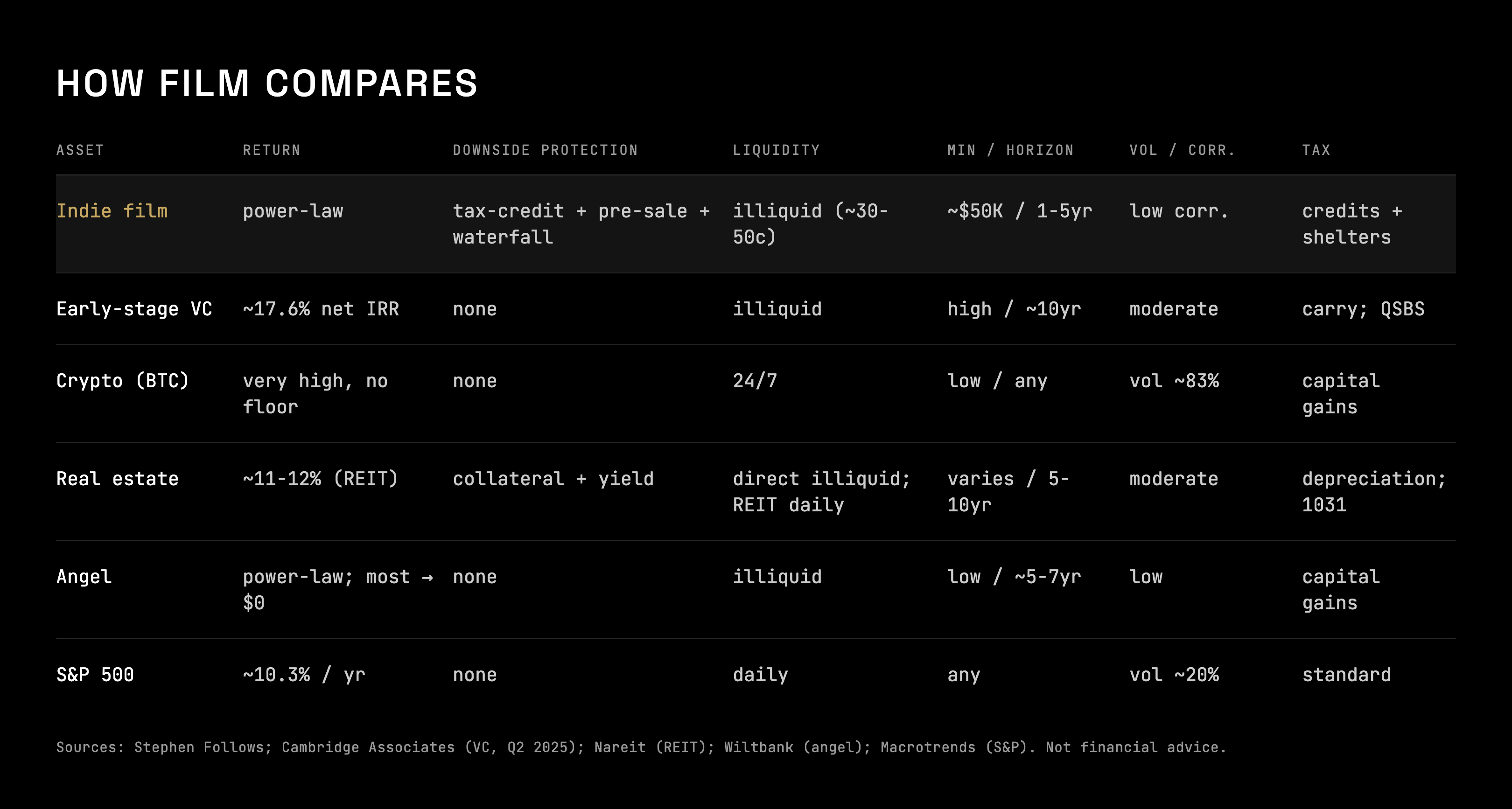

What’s the return profile?

What protects you on the downside?

How liquid is it, can you get out?

What’s the minimum, and how long is your money locked?

How does it move with the public market, and how is it taxed?

Run film through those five and compare it honestly. That’s the table.

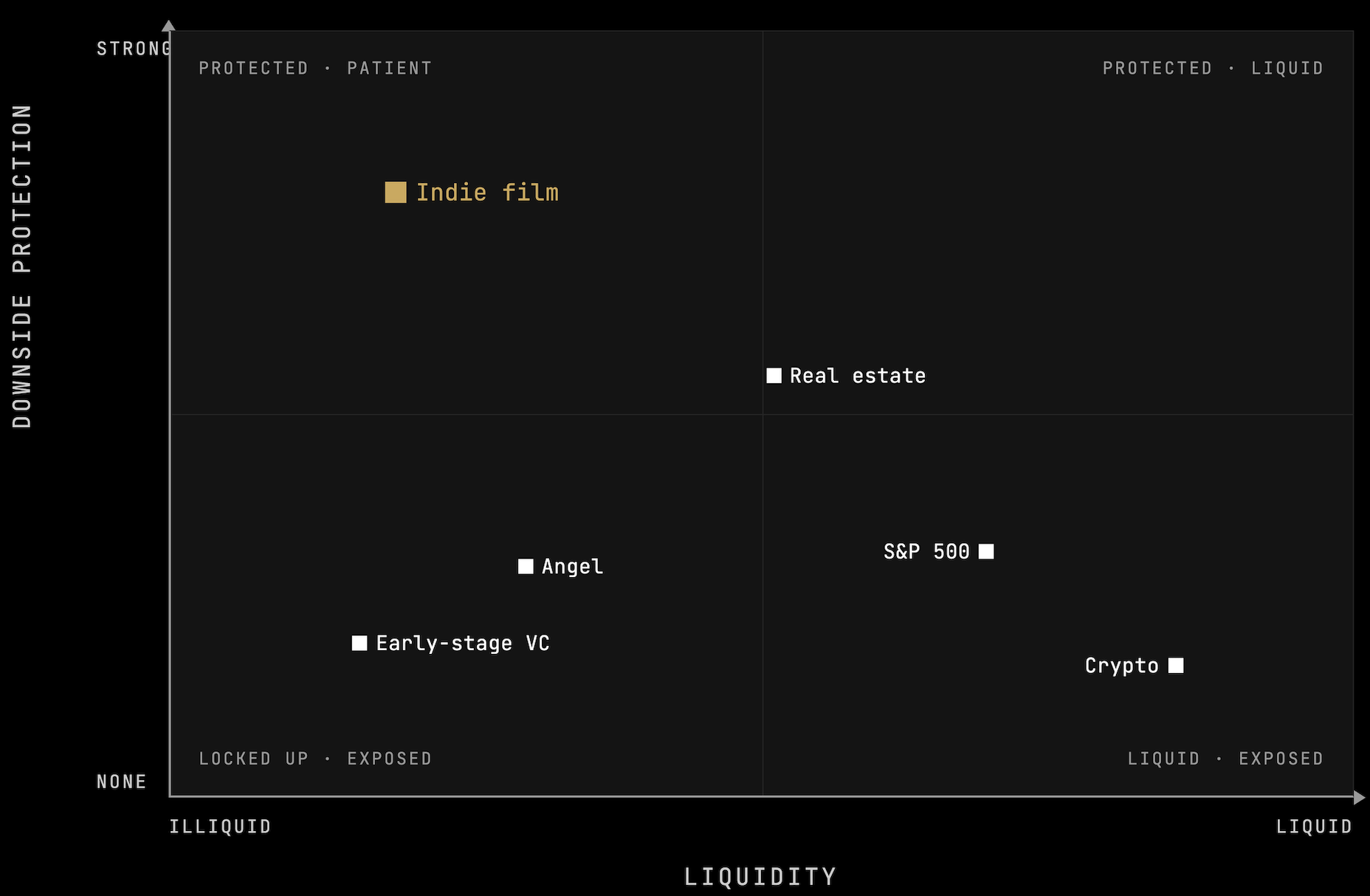

One picture says it faster than the rows. Up means a real floor under your money, right means you can get out. Film sits alone in the protected corner.

Now let me walk the rows that matter.

Return: film is a power-law asset, not an average one

Here’s the trap most film pitches fall into. They quote you an “average return” for film. There isn’t one. No standardized index tracks independent film the way the S&P and Nareit track stocks and REITs. Anyone who hands you a clean average for a film is selling.

So compare honestly. Film belongs in the same bucket as venture capital and angel investing: power-law assets. Most bets return little or nothing. A few outliers pay for everything. You’re not buying an average. You’re buying access to the tail.

Now the number everyone quotes. Stephen Follows ran 37,472 indie films and found that only 3.4% were profitable. That figure shows up in every “should I invest in film” article, and it’s misleading. Count only the films that actually got a theatrical release and it jumps to roughly 33%. Isolate horror over the same window and it’s near 50%. Same data, three very different answers depending on what you actually measure.

And film isn’t one sector, any more than the stock market is. An equity investor splits the market into tech, energy, healthcare. Film splits the same way: drama, auteur, comedy, genre film (horror, action, thriller, sci-fi). Each carries its own numbers, and one sector wins on repeat. Horror. Fear doesn’t need translation. A scare lands the same in any language, which is why genre travels across borders a dialogue-heavy drama never clears. That’s not taste, it’s distribution math.

The tail is real, too. Blair Witch, made for about $60,000, grossed roughly $248 million. Paranormal Activity, made for about $15,000, grossed close to $200 million. Terrifier 3, made for about $2 million, did over $89 million. Same shape as a venture portfolio that catches one unicorn.

Compare that to the other power-law asset on the table. US venture capital posted a pooled net IRR around 17.6% as of mid-2025, per Cambridge Associates, and that headline hides the same brutal distribution underneath. Most funds and most deals don’t drive it. A few do.

The point isn’t “film beats VC.” It doesn’t, on headline return, and I’m not going to pretend it does. The point is that film and venture are the same kind of bet: outlier-driven access plays. If you understand why you’d put money into early-stage venture, you already understand the return shape of film.

Downside: this is where film separates

Where film pulls ahead of its power-law cousins is the floor.

A seed-stage startup has no floor. If it fails, your capital is gone. Crypto has no floor. Angel deals have no floor.

A well-structured film does. Several, actually.

Tax credits. A disciplined producer filming in British Columbia can push the effective return toward 60%. All of it cash back from the government, paid whether or not the film ever finds an audience, and largely before the film’s first screening. I broke down exactly how that works and how far it goes here.

Pre-sales and minimum guarantees. Distributors commit to pay fixed amounts for their territory before the film is shot, against delivery. Contracted cash, not projected revenue.

A completion bond. A bonded film gets finished or the investor gets made whole. That’s an insurance product sitting under your capital.

A first-position waterfall. In a properly papered deal, the equity investor is first money out. Nobody touches a dollar of profit until the investor has recouped their full investment. I get paid after you’re made whole, not before.

Stack those and the math changes. On a $2M Canadian thriller, the tax credits and pre-sales can cover close to 75% of the budget before a single equity dollar goes in. The money actually at risk is meaningfully smaller than the budget on the cover page. No other asset on this list builds in a government-funded floor.

Liquidity: this is where film loses

Film is illiquid. No exchange, no daily price, no easy exit. If you need your money out early, the secondary market for indie film positions is thin and brutal. You might get 30 to 50 cents on the dollar relative to stated value, if you find a buyer at all.

Real estate is illiquid too if you hold it directly, but at least it pays you rent while you wait, and a public REIT trades daily. The S&P you can sell this afternoon. Crypto trades around the clock.

Film pays you nothing while you wait. The wait runs one to five years, sometimes faster, and there are no dividends along the way. Your return, if it comes, comes lumpy and late. If liquidity or income matters to you, film is the wrong asset. I’d rather tell you that now than have you find out in year two.

Correlation: a real edge, stated honestly

Film returns don’t track the stock market. Audiences don’t stop watching movies in a recession. They often watch more. Cinema attendance held up through the Great Depression, and 2008 and 2009 delivered some of the strongest box office of the decade while equities were coming apart. When life gets hard, people spend on escape. There’s even a name for the pattern, the lipstick effect: the small affordable pleasures hold or grow when budgets tighten, and a movie ticket is the cheapest seat in the house.

I’d still love to hand you a correlation coefficient here. I can’t, and neither can anyone honest, because there’s no clean film-return index to run the math on. So treat this as a directional argument, not a number. But the direction is real, and it runs opposite to your equity book.

The risk reframe: film vs the startup you’d back anyway

Put film next to the seed-stage startup, because that’s its real peer.

Both are bets most people lose. Both pay off through a handful of outliers. But the startup has no completion bond, no government credit covering half its costs, no pre-sold revenue, and no waterfall putting your principal first.

Film is the version of that bet with structural protections bolted on. Risky, yes. Uniquely risky, no. The data doesn’t support “film is the riskiest thing you can do with money.” A concentrated single-stock position or a cold seed check has a worse floor.

Who this is for, and who it isn’t

Film fits a specific investor.

You’ve made money in something volatile, tech or crypto or a business exit, and you want a real asset with cultural weight rather than another speculative ticker. You care about what the money makes, not only what it returns, because the film exists in the world and the REIT doesn’t. You can lock up a check from around $50K for one to five years without needing it back.

Film does not fit you if you need liquidity, need income along the way, or can’t hold for the period. No hard feelings. Better to know now.

The return that isn’t on the table

Every asset above returns money or it doesn’t. Film returns something else on top, and no spreadsheet captures it.

You get a credit on the film. You’re on the set if you want to be. You’re at the premiere, on the carpet, at the party. You meet the people who made it, cast included. You can even take a cameo if it suits you, which an indie producer can arrange far more easily than a studio ever could. And you put your name into the cultural record, attached to a film that keeps existing long after a fund’s vintage year is forgotten.

None of that is why a serious investor writes the check. All of it is why, given two comparable bets, they often write this one. Art, wine, and sports hand you a trophy. Film hands you a seat in the room where the thing gets made.

The part that’s mine

Everything above is true for film as a category. Here’s where I differ from the average deal you’d see.

I produce films the way a founder runs a startup. Market first, budget discipline, transparent numbers, a clear path for the money to come back. And I only make films built to do one thing: entertain a real audience while quietly shifting how they see something. That filters for quality, and quality is what travels.

The protections only work if the producer assembling them has done it before and put films into the market that came back. That’s the piece of due diligence no table can show you. It’s the piece worth a conversation.

Where to go from here

This is the map, not the deal. If it changed how you think about where film sits, the job’s done.

I write here every week on how independent film actually works as a business, for the people deciding whether to back one. Subscribe and follow along.

The real version, the actual stack, the waterfall, the numbers on a specific slate, is a conversation, not a download. If you’re weighing whether film belongs in your portfolio, tell me where you’re at and I’ll send the deck and set up a call.

Sources: Stephen Follows (indie film profitability); Cambridge Associates US Venture Capital Index, Q2 2025; Nareit (REIT long-run returns); Wiltbank, Returns to Angel Investors; OfficialData / Macrotrends (S&P 500 since 1926); Creative BC and federal PSTC (tax-credit rates); public box-office records (Blair Witch, Paranormal Activity, Terrifier 3).

*Not financial advice. Film investment carries real risk, including total loss of capital. Consult your own financial advisor and an entertainment lawyer before investing.